Poland’s mandatory e-invoicing through the Krajowy System e-Faktur (KSeF) platform changes how businesses create, submit, validate and receive invoices. Starting February 1, 2026, businesses with annual revenue over 200 million PLN must issue all domestic B2B invoices through KSeF, with full mandatory compliance extending to most businesses by April 2026, according to the European Commission.

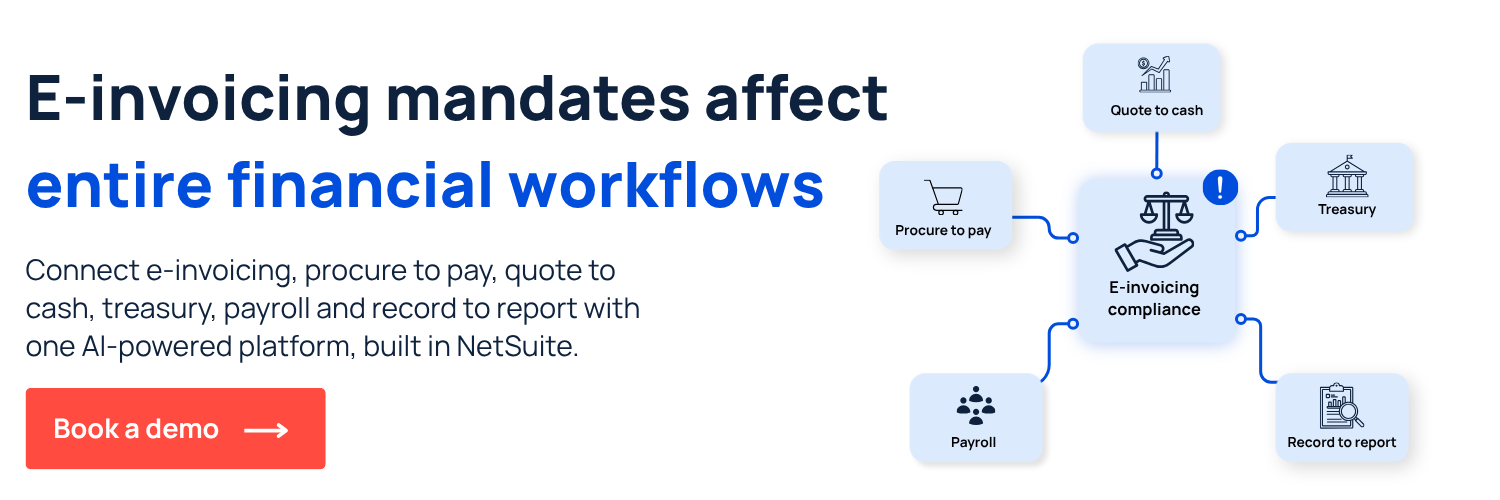

This is different from a small regulatory update. KSeF is a centralized government platform that replaces traditional invoicing methods; invoices no longer flow directly between trading partners, businesses must submit invoices to KSeF for validation, assigned a unique identifier and made available for retrieval through the platform. Finance teams managing NetSuite operations across Poland need compliance strategies that don’t fragment invoice processing across disconnected systems.

Key highlights:

- E-invoicing in Poland requires structured invoices through KSeF, Poland’s centralized government platform that validates, identifies and stores all domestic B2B invoices.

- Poland stands out from other European mandates because KSeF is a mandatory government clearance platform, not an optional exchange format.

- Compliance affects both issuing and receiving invoices, raising the bar for ERP integration, AP workflow automation, AR process readiness and tax reporting accuracy.

What e-invoicing in Poland actually means

E-invoicing Poland is the mandatory use of the Krajowy System e-Faktur (KSeF) for in-scope business-to-business invoice transactions. KSeF is Poland’s national electronic invoicing system that validates, registers and stores structured invoices in a centralized government platform.

So, what’s happening?

Poland’s e-invoicing KSeF updates mean that KSeF is becoming the mandated environment in phases between February 2026 and January 2027 for VAT‑registered businesses in scope. Traditional paper invoices and PDF invoices sent via email are no longer valid for in-scope domestic B2B transactions. Every invoice for in-scope transactions now must be issued in structured XML format conforming to the FA(3) schema, submitted to KSeF for validation and assigned a unique KSeF identification number before it becomes legally effective.

What makes Poland different:

- Centralized government platform: Unlike France’s approved platform (PA) model, for example, Poland requires invoices to flow through a single government-operated system.

- Structured invoice requirements: Invoices must conform to the FA(3) schema with precise field definitions and validation rules, according to Polish government materials.

- Mandatory operational process changes: Buyers retrieve invoices from KSeF rather than receiving them directly from suppliers, disrupting current AP workflows.

- Stronger auditability and reporting logic: Tax authorities gain real-time access to invoice data, increasing transparency and compliance pressure.

- Higher integration burden for ERP-led organizations: Finance teams must connect tools like NetSuite to KSeF, implement validation workflows and redesign AP/AR processes to accommodate platform-based invoice exchange.

What changed in Poland’s KSeF rollout

Poland’s path to e-invoicing has been marked by multiple delays and refinements. Understanding what changed and why those changes matter helps finance teams prepare appropriately.

The late-2025 changes that still matter now

Poland’s e-invoicing KSeF updates in October and November 2025 centered on finalizing the technical framework. In August 2025, Poland’s president signed the law establishing KSeF as mandatory from February 1, 2026.

The Ministry has released the final FA(3) schema, published KSeF 2.0 API documentation, opened the test environment and issued four implementing regulations.

Why those changes raised the stakes for businesses

The finalization of the KSeF update created narrow windows for system integration, data cleanup and user training. This means more pressure on process automation, more need for integration and testing and higher dependency on ERP capabilities for NetSuite teams.

KSeF key dates and milestones

Sequencing readiness against deadlines and transition periods is one of the hardest parts of the Poland e-invoicing KSeF update news. Finance teams must coordinate technical integration, process redesign and user training across compressed timeframes.

Phased implementation creates different timelines for SMBs versus large enterprises:

- Large taxpayers (PLN 200 million+ turnover) must comply by February 1, 2026.

- Most VAT-registered businesses by April 1, 2026.

- Micro-entrepreneurs (monthly sales under PLN 10,000) have until January 1, 2027.

- However, in-scope businesses must be able to receive e-invoices through KSeF starting February 1, 2026.

What these dates mean in practice

- Finance needs process mapping to identify KSeF requirements.

- IT needs integration readiness to connect NetSuite to KSeF API.

- Tax teams need control visibility to ensure FA(3) schema compliance.

- Teams need training on authentication, invoice retrieval and error handling.

- Leadership needs a transition plan accounting for the February 2026 receiving requirement and phased issuing requirement.

Which transactions and businesses are affected by Poland e-invoicing regulations?

Poland’s KSeF mandate applies broadly to domestic B2B transactions but creates different obligations, depending on transaction type and business profile.

B2B

- Primary focus of the Poland mandate

- Structured invoice compliance through KSeF

- Biggest impact on enterprise finance operations

B2G

- Public sector invoicing has its own workflow and reporting implications

- Organizations need to understand how KSeF intersects with public invoice handling

- Organizations can process invoices through either KSeF or PEF

B2C

- Not the main mandatory KSeF use case today

- Still relevant for future-watch discussions and customer experience implications

Which companies are most affected:

- Large B2B organizations face the earliest deadlines

- Multi-entity groups operating multiple Polish subsidiaries must coordinate implementation across all entities

- Companies with high invoice volume need robust automation to handle KSeF at scale

- Organizations operating across borders must distinguish between domestic Polish invoices (KSeF required) and cross-border transactions

How KSeF works in practice

Understanding how KSeF operates helps finance teams design integration strategies that support compliance without operational disruption.

Platform structure and invoice identification

KSeF is a centralized government platform operated by Poland’s Ministry of Finance, requiring all invoices to undergo automated validation against the FA(3) schema. Only invoices passing validation are registered, timestamped and assigned a unique KSeF identification number.

This identifier confirms the invoice was legally issued, provides traceability for tax authorities, must be included in bank payment references starting August 2026 and links the invoice to KSeF’s 10-year archiving repository.

Polish buyers retrieve invoices from KSeF using their credentials or grant access to accounting firms through delegation mechanisms. Foreign recipients receive invoices outside the system, but those invoices still need KSeF identifiers.

KSeF EDI, formats, and technical rules

KSeF requires invoices in structured format conforming to the FA(3) logical structure. This schema replaced FA(2) as part of the change, and includes expanded fields for payment information, VAT rate codes, attachments and invoice metadata.

KSeF electronic data interchange (EDI) are capabilities that allow systems to submit and retrieve invoices programmatically through the KSeF API. Organizations with high invoice volumes need EDI integration between their ERP and KSeF.

ERP integration options

Finance teams monitoring KSeF news in Poland have several approaches for connecting NetSuite to KSeF:

- Direct integration: Build API connections using custom code, maintaining control but requiring significant development

- Middleware: Use integration platforms between NetSuite and KSeF, adding another system layer

- Manual workflows: Use KSeF web portal for manual entry

- Native ERP extensions: Built-in-NetSuite solutions provide KSeF connectivity directly in the ERP.

How businesses using NetSuite can comply with KSeF

Poland’s mandate changes how invoices are created, received, validated, approved, stored and monitored across the entire procure-to-pay and order-to-cash lifecycle. Here’s how businesses in NetSuite can comply with the e-invoicing regulations in Poland:

Outbound invoicing

Creating and submitting invoices through KSeF requires NetSuite to generate FA(3)-compliant data and handle validation responses:

- Create compliant invoices by ensuring NetSuite records contain all FA(3) schema fields including payment links, KSeF identifiers and VAT classifications

- Submit through KSeF using authentication (certificates or seals), API integration that formats invoice data into FA(3) XML and transmission to the platform for validation

- Track invoice status by monitoring whether invoices passed validation, received KSeF identification numbers and are available for buyer retrieval

- Handle exceptions including validation failures, offline mode usage during system outages and resubmission of corrected invoices

Inbound invoicing and AP impact

Receiving supplier invoices from KSeF can change AP workflows because invoices arrive as structured XML data rather than email attachments:

- Receive supplier invoices through KSeF by configuring AP team access through portal login or delegation to accounting software providers

- Validate and route for approval using systems that retrieve invoices from KSeF, convert XML into readable formats, match to purchase orders and route through approval hierarchies

- Connect inbound compliance to AP operations with solutions that maintain invoice processing inside NetSuite rather than fragmenting workflows across external tools

Data, controls, and auditability

The FA(3) schema and real-time tax authority access create higher standards for data accuracy and internal controls:

- Required data completeness includes specific VAT rate codes, payment method classifications and buyer/seller identification through tax IDs (NIP)

- Internal controls need strengthening around KSeF authentication permissions, approval hierarchies before invoice submission and validation error escalation processes

- Documentation discipline matters because tax authorities have real-time KSeF access, meaning discrepancies create immediate audit exposure

- Retention and audit readiness leverage KSeF's 10-year archiving but businesses still need searchable records linking KSeF identifiers to contracts, purchase orders and payment records

Training and change management

Successful KSeF implementation requires coordination across finance, tax and IT with tailored training for each function:

- Identify user groups including AR teams (issuing invoices), AP teams (retrieving supplier invoices), tax teams (schema compliance) and IT teams (authentication and integration)

- Tailor training for finance and IT because responsibilities differ – finance focuses on data quality and validation requirements while IT focuses on API integration and error handling

- Schedule refreshers as KSeF evolves with schema updates, new features and validation rule changes

- Communicate process changes to suppliers and customers about new invoice delivery methods and KSeF identifier requirements

- Define ongoing support for troubleshooting validation errors, managing certificate renewals and coordinating with the Ministry of Finance

How NetSuite teams should prepare for KSeF e-invoicing in Poland

Finance and IT leaders managing NetSuite across Poland need practical e-invoicing implementation steps:

- Assess current invoicing flows: Document how invoices are generated today (manual entry, automated from sales orders and recurring billing) and where validation happens. On the AP side, map how supplier invoices arrive and flow through approval hierarchies.

- Identify where KSeF requirements affect data and controls: The FA(3) schema mandates fields that may not exist in current NetSuite configurations. Determine what data cleanup is required, what new fields must be added and what validation rules should catch errors before submission.

- Decide how ERP integration will work: Will IT build direct API connections, purchase middleware or implement a NetSuite solution like ZoneCapture? Who manages KSeF certificates and authentication?

- Redesign workflows: AR teams need procedures for submitting invoices to KSeF and tracking validation status. AP teams need procedures for retrieving supplier invoices from KSeF and matching to purchase orders. Both need escalation paths for validation errors.

- Train finance, tax and IT teams together: KSeF crosses functional boundaries. Finance owns compliance, tax validates schema requirements and IT manages authentication.

- Build an ongoing compliance process: Finance teams need monitoring processes for regulatory updates and testing procedures for schema changes.

Take the next step toward Poland e-invoicing compliance

Poland’s KSeF mandate changes invoice processing for businesses operating in Poland. Finance teams need solutions that deliver compliance without fragmenting workflows across disconnected systems.

When finance teams search for companies that support KSeF e-invoicing in Poland, they need solutions that can generate FA(3)-compliant XML, authenticate to KSeF securely and integrate KSeF identifiers into accounting workflows. Poland is phasing in mandatory structured e-invoicing through KSeF beginning in 2026, with deadlines varying by taxpayer size. Businesses operating in Poland should assess invoicing processes, data readiness, and integration needs early while continuing to monitor official guidance.