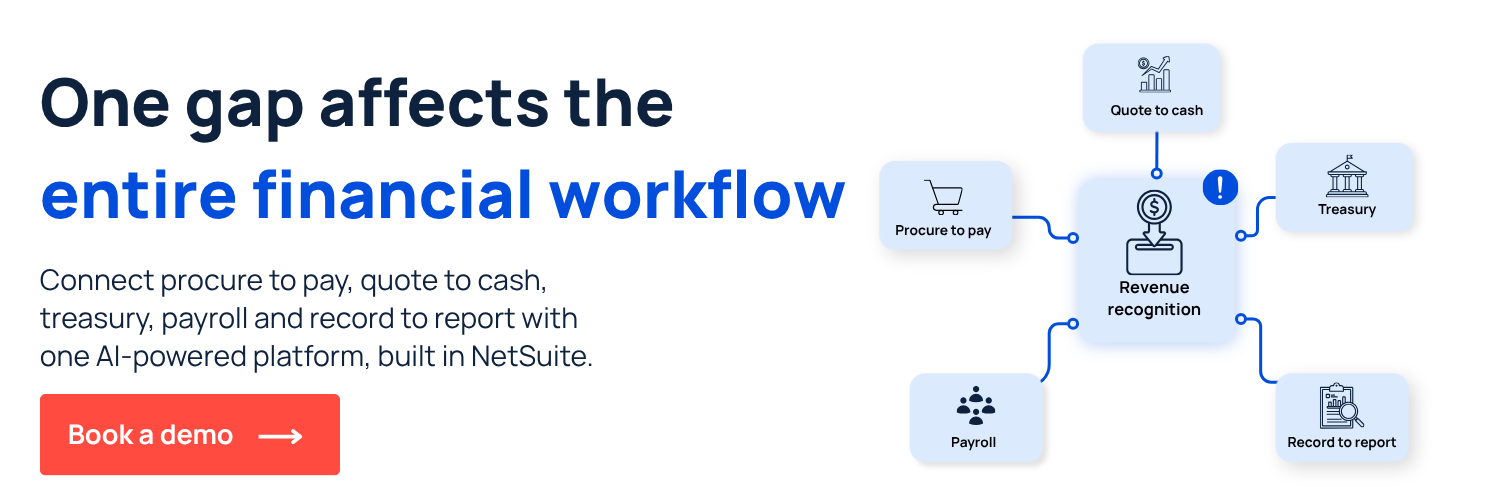

What is revenue recognition?

Take the ZoneBilling product tour →Revenue recognition is the accounting principle that determines when a company records revenue in its financial statements – specifically, that revenue should be recognized when it is earned (when performance obligations to the customer are satisfied), not simply when cash is received or an invoice is sent.

Under U.S. Generally Accepted Accounting Principles (GAAP), which houses ASC 606 regulations and International Financial Reporting Standards (IFRS) 15, this principle applies to all revenue-generating businesses. Revenue recognition impact is greatest for companies with subscription billing, multi-element contracts or long-term service agreements, where the timing of cash receipt and earned revenue frequently diverge.

Why revenue recognition matters

A customer pays $96,000 upfront for an annual SaaS subscription on October 1. The cash hits the bank and the sales team celebrates. Then Finance adds $96,000 to deferred revenue and begins recognizing $8,000 per month. But in February, the customer upgrades their plan. The contract value increases to $120,000 and the remaining performance obligation changes. Finance recalculates the revenue schedule, adjusts the deferred balance and ensures the amendment is reflected in the current period – not the period it was signed or the period it was invoiced.

Revenue recognition directly affects the accuracy of the income statement. Recognizing revenue too early overstates performance and creates restatement risk. Recognizing it too late understates the business and distorts period-over-period comparisons.

Revenue recognition principles

Understanding rev rec’s core principles helps finance teams automate it for cleaner compliance workflows.

The core principle

Under ASC 606 and IFRS 15, revenue should be recognized to depict the transfer of goods or services to customers in an amount that reflects the consideration the company expects to receive. In plain terms: recognize revenue when you’ve delivered what you promised, in proportion to what you’ve delivered.

Point-in-time vs. over-time recognition

Revenue is recognized either at a point in time or over a period of time, depending on when control of the goods or service transfers to the customer. A software license delivered on a specific date is recognized at that point. A SaaS subscription providing continuous access over 12 months is recognized ratably – typically monthly – as the service is delivered.

ASC 606 and IFRS 15

ASC 606 under U.S. GAAP and IFRS 15 that governs international accounting standards share a common five-step framework: identify the contract, identify performance obligations, determine the transaction price, allocate the price to obligations and recognize revenue as obligations are satisfied. What matters operationally is that both standards require contracts to be analyzed at the obligation level, not the invoice level.

Common revenue recognition challenges for finance teams

Most rev rec problems happen when contract data, billing events and recognition schedules live in different systems and don’t talk to each other.

- Contracts aren’t entered at the obligation level. When deals are logged as a single line item rather than broken into distinct performance obligations, the system has no basis to generate an accurate recognition schedule. The revenue team ends up building it manually.

- Contract modifications require manual recalculation. An upgrade, a seat reduction, an early cancellation – each one changes the remaining performance obligation and the deferred revenue balance. Without system automation, every modification means someone rebuilding the schedule by hand.

- Billing and recognition run in separate systems. When the billing platform and the ERP don’t share data in real time, the revenue team is reconciling two ledgers at close instead of simply reviewing one.

- Usage-based charges don’t fit neatly into static schedules. Variable consumption models generate recognition events that change each period. Maintaining these manually when the business scales isn’t sustainable.

- Journal entries are still posted by hand. When recognition dates arrive, someone has to create and post the entries. In high-volume environments, this is where errors accumulate and close timelines stretch.

ASC 606 disclosures are built from separate workbooks. Disaggregated revenue, contract asset and liability balances, remaining performance obligations – these disclosures are often assembled manually from data that already exists in the ERP, just not in a reportable format.

How teams improve revenue recognition

Improving revenue recognition means replacing manual schedule maintenance with a system-enforced process that updates automatically when contracts change. Here’s how finance teams do it:

- Map contracts to performance obligations at the point of entry: Configure the ERP to capture obligation-level contract data when a deal is created, so recognition schedules can generate automatically without manual setup.

- Automate recognition schedule creation: When a contract is entered, the system should generate the full recognition schedule – including deferred revenue waterfall – without requiring manual journal entry setup.

- Handle contract modifications automatically in the current period: When a customer upgrades, cancels or modifies their contract, the recognition schedule should update in the current period without manual recalculation by the revenue team.

- Connect billing events to recognition triggers: Link billing system data to recognition schedule updates so that usage-based charges, renewals and amendments flow through to recognition automatically.

- Run journal entries on schedule without manual intervention: Recognized revenue journal entries should post automatically on each recognition date, eliminating the month-end manual journal entry process.

- Generate close-ready disclosure reports from the same data: ASC 606 disclosures like disaggregated revenue, contract balances and remaining performance obligations should auto-populate from the same data that drives recognition, not from separate manual workbooks.

How ZoneBilling improves and automates revenue recognition

ZoneBilling connects billing events directly to NetSuite’s Advanced Revenue Management module, automating revenue schedule creation and updates, handling contract modifications and usage-based charges, and maintaining a complete audit trail for every recognition event.

Core capabilities include:

- Wraparound revenue recognition that enhances NetSuite ARM rather than replacing it.

- ASC 606 and IFRS 15 compliance automation that manages performance obligation analysis, allocation and recognition at the contract level, not the invoice level.

- Automated contract modification handling that updates automatically in the current period without manual recalculation

- Multiple performance obligation (MPO) allocation to split transaction price across distinct obligations using SSP logic, with retrospective and prospective re-allocation supported.

- Automated journal entry posting so recognized revenue entries post on schedule without manual intervention, removing the month-end journal entry process from the close checklist

Book a personalized demo with an expert to explore ZoneBilling’s capabilities in NetSuite.

.avif)

.png)