Greece made structured electronic invoicing mandatory for domestic B2B transactions under Law 5222/2025. Phased compliances started in March 2026 for large businesses with more than €1 million in 2023 revenues, and other businesses will follow in October 2026.

Your business’s invoice data quality will also directly determine whether myDATA accepts or rejects your submissions, and your exception handling workflows need to work inside your ERP. These are the regulatory requirements, myDATA’s clearance mechanics, your enterprise resource planning (ERP) workflow changes and the day-to-day accounts payable (AP) and accounts receivable (AR) impacts that matter to finance, tax and IT teams.

Key highlights

- Law 5222/2025 Greece e-invoicing replaces voluntary e-invoicing with mandatory structured invoicing for domestic B2B transactions.

- MyDATA Greece validates every invoice, assigns unique MARK identifiers and rejects invoices with data errors or missing classification codes.

- Greece e-invoicing mandates change how invoices are issued, received, validated and archived across your AP, AR, tax and ERP workflows – this touches everyone, not just your tax team

What Law 5222/2025 changes for Greece e-invoicing mandates

Law 5222/2025 transforms Greece e-invoicing from voluntary practice to mandatory requirement for domestic business-to-business transactions. Published in July 2025, the law amends Article 14 of Law 4308/2014 (Greek Accounting Standards) and establishes structured electronic invoicing as the legal standard for businesses established in Greece.

The change goes beyond adding a compliance checkbox. Here’s what’s changing:

- In-scope invoice data must be transmitted through approved channels and associated with the required myDATA identifiers, such as MARK, where applicable. Errors or missing data can create compliance issues, delays and exception handling work

- Buyers retrieve invoices through myDATA or certified provider transmission instead of email

- Finance teams must populate EN 16931-compliant fields plus Greek classification codes that most ERP systems don’t capture today

Here’s a quick overview, according to the European Commission and Greece’s Independent Authority for Public Revenue:

Why finance systems teams need to be involved

These aren’t just small changes. When invoice data fails validation, the invoice doesn’t exist legally, which blocks revenue recognition, delays customer billing and creates AP exceptions when supplier invoices can’t be processed.

As a result, finance systems teams shouldn’t treat this as a simple myDATA connector project. Here’s what needs to happen:

- Invoice generation workflows need redesigned to populate Greek classification codes before creation

- Validation error handling needs to catch problems before invoices reach customers

- Retry logic for failed transmissions becomes critical infrastructure

- Audit trails must link MARK identifiers back to accounting records without manual reconciliation

Non‑compliance with e‑invoicing and myDATA transmission obligations can trigger penalties. Finance teams should review the latest AADE guidance or seek local advice to confirm the exact penalty amounts and thresholds that apply to their business.

Greece e-invoicing scope and timeline

The Greece e-invoicing mandate applies to businesses established in Greece for domestic B2B transactions and sales to non-EU third countries. The two-phase timeline gives large businesses a head start but shortens implementation windows for everyone else.

These are the key dates that the AADE published, accurate as of June 4, 2026:

The gradual implementation periods let businesses run parallel systems while building out full compliance. Finance teams should verify the latest AADE guidance before finalizing go-live plans, as transitional mechanics may continue to change.

Finance teams should verify the latest AADE guidance before finalizing go-live plans, as transitional mechanics may continue to evolve based on implementation feedback from Phase A businesses.

Who is in scope?

All businesses established in Greece with VAT registration engaging in domestic B2B transactions fall under the mandate. That includes large enterprises with EUR 1 million+ gross revenues in 2023 (Phase A), SMEs and micro-enterprises (Phase B), and foreign businesses with permanent establishments in Greece conducting domestic transactions.

Limited exemptions apply for digitally excluded taxpayers who lack technical infrastructure, but most businesses operating ERP systems like NetSuite fall under mandatory compliance.

Here’s an overview:

Keep in mind that all domestic recipients will be expected to accept and process structured e‑invoices once the mandate applies, including invoices received from suppliers that enter the regime earlier in Phase A.

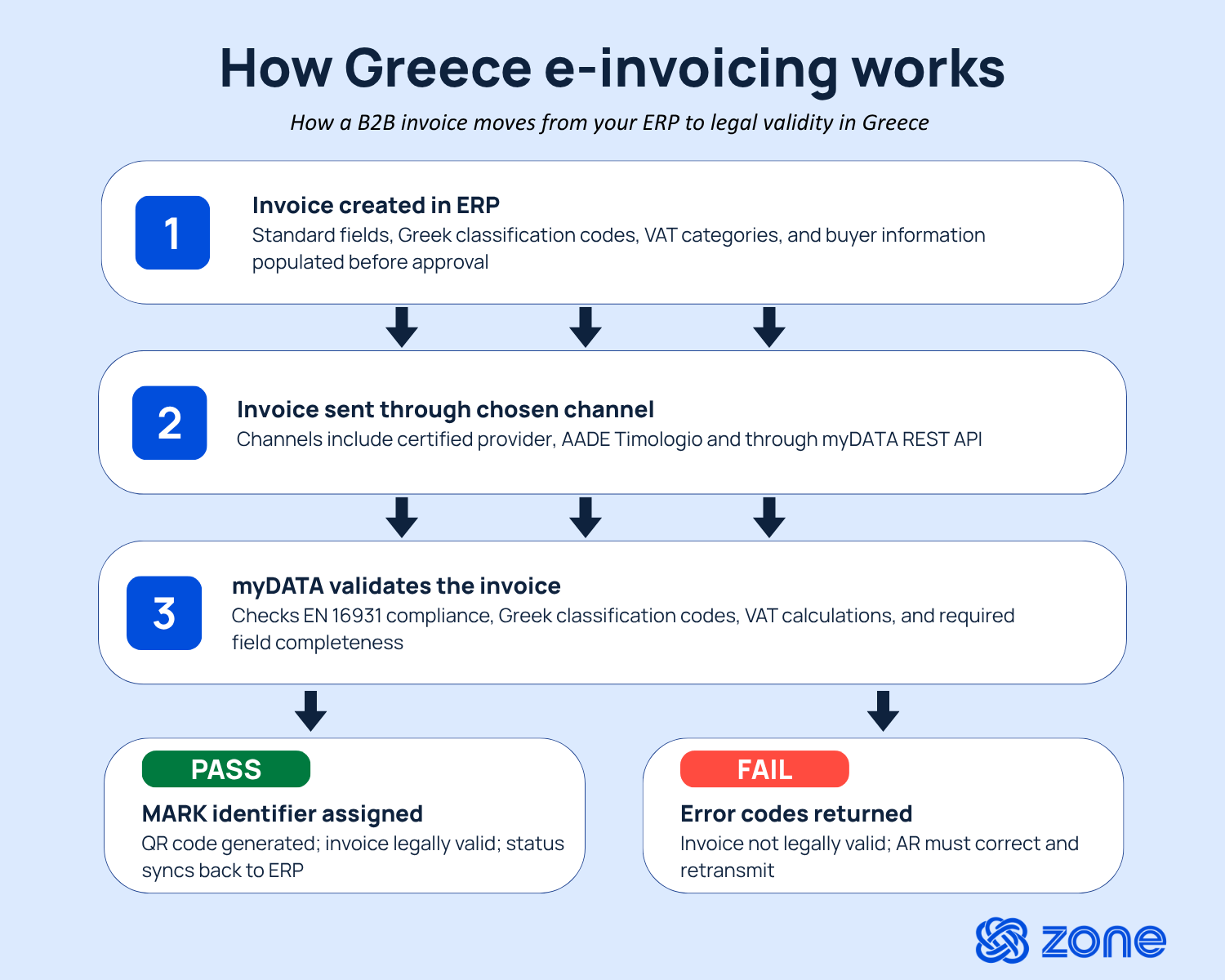

How myDATA works in Greece

MyDATA is AADE’s centralized clearance platform. Every domestic B2B invoice must pass through myDATA validation. Here’s how the data flows and where things break when it comes to the new setup for e-invoicing in Greece.

What Greece’s myDATA receives

MyDATA receives structured invoice data from issuers through one of three channels: certified providers, AADE’s Timologio application or direct API integration. The platform validates that data against EN 16931 requirements and Greek-specific classification codes covering income categories, VAT categories, invoice types and payment methods. It checks for required field completeness, VAT calculation accuracy, classification code validity and format compliance.

When an invoice passes validation, myDATA assigns a registration number (MARK) and returns it to the issuer. This MARK must appear on the document you provide to the buyer.

How invoice data moves

The flow starts when your finance team creates an invoice, populating standard fields (line items, amounts, VAT) along with the Greek classification codes myDATA requires. That data gets transmitted to myDATA through your chosen channel, which would either be a certified provider, Timologio or direct REST API.

If the invoice passes validation, it gets a MARK identifier and QR code. If it fails, you get error codes back. Either way, that response needs to flow back into your ERP so invoice status stays current, payment matching works and your audit trail remains intact.

Once validated, the invoice reaches the buyer through myDATA retrieval, certified provider transmission or as a digital file with the QR code embedded.

What failed submissions mean for finance teams

Failed submissions hit AR and AP differently, but both create real operational pain. On the outbound side, a failed validation means revenue recognition gets delayed, AR can’t collect payment and month-end close stretches when validation errors prevent invoice finalization.

On the inbound side, failed supplier invoices block three-way matching and stall approval routing until the supplier corrects and retransmits. Accruals lose accuracy when invoices are stuck pending validation at period-end, and AP teams have limited ability to accelerate the fix.

Making this worse, tax authorities have real-time visibility into myDATA transmissions. Any discrepancy between what you’ve transmitted and what you report on VAT returns creates immediate audit exposure.

Implementation options for Greece e-invoicing

Getting to myDATA compliance involves more than choosing a certified provider. Finance and ERP teams need to sort out data requirements, figure out who owns what in the new workflow and build exception handling before go-live.

Data and document requirements

Greece e-invoicing requires invoices to include EN 16931 standard fields plus Greek-specific classification codes. Your ERP must populate:

- Standard invoice elements: Seller/buyer identification (VAT numbers, addresses), invoice number and date, line item descriptions and amounts, VAT rates and amounts, payment terms

- Greek classification codes: Income classification category, VAT category codes, invoice type codes, payment method codes, withholding tax information where applicable

- MARKplacement: After successful myDATA validation, the MARK identifier and QR code must appear on the invoice document provided to buyers

Workflow ownership and exception handling

Greece e-invoicing creates new workflow touchpoints that need clear ownership. Without defined roles, validation failures sit in limbo while AR, tax and IT teams point fingers.

Before myDATA transmission:

- AR teams own invoice creation accuracy, including correct classification codes, VAT calculations and complete buyer information

- Tax teams validate classification code assignments, especially for complex transactions involving multiple revenue types or special VAT treatments

- IT teams maintain certified provider connections, API authentication and error logging

During validation and exception handling:

- AR teams monitor validation failures for outbound invoices, correct errors and retransmit

- AP teams track validation status for inbound supplier invoices and delay payment processing until invoices receive MARK identifiers

- Tax teams resolve classification code disputes and interpret AADE validation error messages

After successful transmission:

- AR teams ensure MARK identifiers appear on invoice documents and are stored in ERP records

- AP teams verify supplier invoice MARK identifiers before processing payments

- Finance teams reconcile myDATA transmission logs to accounting records during month-end close

The key design principle here is to separate invoice generation from myDATA transmission in your ERP architecture. AR teams shouldn’t discover classification code errors at the point of approval. Validation checks should run while invoices are still in draft, and exception queues should route failures to the right owner based on error type. Data quality issues go to AR, classification codes to tax and technical failures to IT.

Greece e-invoicing readiness checklist

Finance and IT leaders in Greece should complete these e-invoicing implementation steps before their mandatory compliance date:

- Confirm whether Greek entities and domestic B2B flows are in scope

- Review invoice data quality, VAT treatment and customer/supplier master data

- Understand available transmission options: certified providers, AADE tools or direct integration

- Assign internal ownership across finance, tax and IT

- Monitor AADE guidance as implementation details evolve

- Engage tax, ERP or implementation partners early

Common Greece e-invoicing compliance barriers

The blockers that slow Greece e-invoicing implementation are predictable. Most come down to disconnected tooling, weak invoice data, unclear ownership and limited visibility into what’s failing and why.

Here’s what finance teams run into most often (and what better looks like):

Zone & Co is monitoring e-invoicing developments across Europe, including Greece, as requirements continue to evolve. Businesses with Greek entities should begin assessing their invoice workflows, data readiness and compliance obligations now, while confirming final requirements with local tax advisors or official AADE guidance.