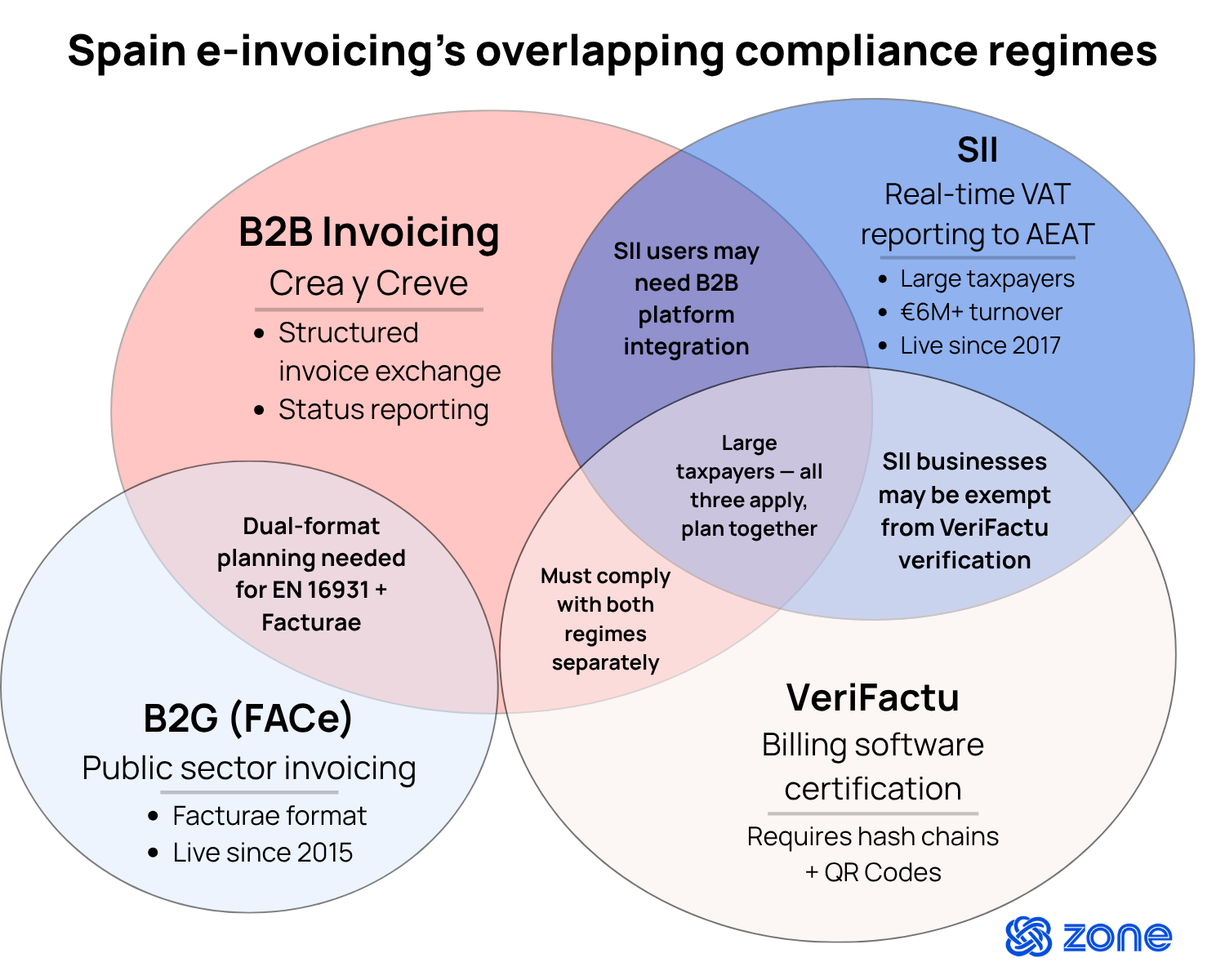

Spain’s e-invoicing timeline can be more complex to pin down compared to other European mandates because it involves three overlapping regimes that affect different parts of finance operations:

- The B2B e-invoicing mandate under Royal Decree 238/2026

- VeriFactu’s software certification requirements under Royal Decree 1007/2023

- The existing Suministro Inmediato de Información (SII) real-time VAT reporting system

Each of these regulations have their own scope, deadlines and technical requirements. Treating them as one generic, singular Spain e-invoicing project will likely result in finance teams ending up with fragmented tooling and missed deadlines.

The regulatory picture sharpened significantly in early 2026. Royal Decree 238/2026 was published on March 31, 2026, establishing the B2B framework. VeriFactu deadlines, after multiple postponements, are set for January and July 2027. And with software adaptation deadlines approaching, recipient-side obligations change how your accounts payable (AP) team works and payment-status reporting adds new data requirements.

Key highlights:

- Spain e-invoicing involves three distinct compliance regimes, each with different scope, timelines and technical requirements.

- The B2B mandate under Royal Decree 238/2026 requires structured invoice exchange through public or private platforms, plus mandatory invoice status and payment date reporting.

- VeriFactu is an entirely separate software certification regime that ensures your billing system produces tamper-proof, traceable invoice records.

- Finance teams need to plan for adoption together but implement them separately, mapping which obligations apply to their business before making technology decisions.

Spain e-invoicing timeline at a glance

Spain’s B2B e-invoicing mandate, VeriFactu and SII all run on different clocks. Some are already finalized, while others are pending.

Here’s where each one stands as of June 4, 2026, according to Boletín Oficial del Estado (BOE) and European Commission information:

What’s finalized for Spain e-invoicing

These regulations are already finalized:

- Royal Decree 238/2026 is published and in force

- The B2B e-invoicing framework is legally established

- VeriFactu deadlines are set at January 1, 2027 for corporate taxpayers and July 1, 2027 for all other tax payers

- SII and B2G obligations are already operational with businesses submitting e-invoicing through Punto General de Entrada de Facturas Electrónicas (FACe)

What’s still pending

Spain’s mandatory B2B e-invoicing regime is not yet in effect. While the underlying legislation (Law 18/2022 and Royal Decree 238/2026) is in force, the Ministerial Order that defines the public platform’s technical specifications — and formally starts the compliance clock — remains unpublished as of mid-2026. Businesses should not assume any specific deadline until that order is confirmed.

Based on the current draft, entry into force is targeted for October 1, 2026, which would give larger businesses (turnover above €8 million) until around October 2027, and smaller businesses until around October 2028. However, these dates are indicative only and subject to change pending final publication.

What finance teams can act on now

You don’t need final dates to start preparing. Here’s what to do now:

- Map which of the three regimes apply to your business

- Confirm your invoicing software handles VeriFactu requirements

- Assess your data quality for B2B e-invoicing fields

- Review your SII reporting workflows for overlap with new B2B status reporting

- Evaluate platform options (including AEAT’s public solution or private interoperable platforms) before the Ministerial Order narrows your implementation window

Which businesses are affected by Spain’s B2B e-invoicing mandate

The B2B e-invoicing mandate under Royal Decree 238/2026 applies to businesses and professionals conducting B2B transactions in Spain. Company size determines your deadline, and recipient-side obligations change the operating model in ways most teams don’t initially expect.

Spain’s B2B e-invoicing mandate scope

All entrepreneurs and professionals operating in Spain must issue, transmit and receive structured electronic invoices for B2B transactions. The mandate covers:

- Invoice exchange through AEAT’s public platform or certified private platforms

- Mandatory reporting of invoice status

- Payment date reporting

Crucially, PDF-only invoices will no longer satisfy B2B requirements once deadlines take effect. These are the deadlines based on business size, according to the BOE:

Recipient and payment-status obligations

This is where Spain’s mandate differs from some other European e-invoicing regimes. It’s not just about issuing invoices, as recipients have active obligations too.

Under Royal Decree 238/2026, invoice recipients must communicate rejection, acceptance and the date of full payment electronically to the public platform. Recipients may also need to report the payment due date, and in some cases the date goods were received or services performed, where these are relevant to calculating payment periods under Spain’s anti-late-payment rules.

Payment date reporting is also mandatory. When you pay an invoice, that date must be transmitted through the platform. In addition to enforcing VAT compliance, this mandate seeks to combat late payments.

For AP teams, this means payment processing workflows need to connect to the e-invoicing platform so payment dates flow to AEAT automatically.

What is VeriFactu in Spain?

VeriFactu Spain is one of the most misunderstood parts of the Spanish compliance landscape. It’s not an e-invoicing mandate; it’s a billing software certification regime designed to prevent tax fraud by ensuring invoice records are tamper-proof and traceable.

What VeriFactu is designed to do

VeriFactu (formally the SIF – Sistema Informático de Facturación) was introduced under Spain’s Anti-Fraud Law 11/2021 and specified by Royal Decree 1007/2023. It requires that the software you use to generate invoices produces records that are:

- Sequentially chained with digital fingerprints (hash chains)

- Timestamped

- Including a QR code for verification

- Cannot be altered after issuance

The system gives AEAT a way to verify that no invoices have been deleted, modified or hidden after creation. Businesses can either submit billing records directly to AEAT (the “VeriFactu” option) or use certified billing systems that store records locally with the required integrity controls (the “SIF” option).

Software requirements that matter

VeriFactu’s deadlines are the most immediate, and your invoicing software needs to meet all of these:

- Spain has intentionally begun phasing out non-compliant invoicing software

- Corporate taxpayers must use VeriFactu-compliant systems by January 1, 2027

- Self-employed and other taxpayers must comply by July 1, 2027

- Software must produce chained hash records, QR codes and timestamps for every invoice

- Records must be unalterable once created

Businesses already complying with SII are exempt from VeriFactu’s software certification requirements. Since SII already provides AEAT with real-time invoice data, the anti-fraud protections VeriFactu addresses are already covered.

VeriFactu vs. B2B e-invoicing

These two regimes are complementary, not interchangeable. A single business may be subject to both simultaneously.

How Spain e-invoicing relates to SII and B2G invoicing

Spain’s overlapping compliance regimes create confusion because they use similar terminology but serve different purposes. Separating them by what they do and who they affect operationally makes the planning clearer.

SII is already live. However, it doesn’t dictate invoice format. A business under SII can still issue PDF invoices and report the data separately. The new B2B mandate changes that by requiring structured formats for the invoices themselves.

Meanwhile, B2G invoicing through FACe uses the Facturae format, which differs from the EN 16931/UBL format the B2B mandate requires. As a result, finance teams should plan for format coexistence rather than assuming one solution covers both.

What finance and ERP teams should do before Spain deadlines tighten

Waiting for the Ministerial Order before starting preparation is one of the most common mistakes. VeriFactu deadlines are already set, data quality issues take months to resolve and platform evaluation requires understanding your transaction landscape.

Software and data readiness

When you’re getting your software and data ready for upcoming Spain deadlines, start with what you know.

Your invoicing software needs to be VeriFactu-compliant by January 2027 (corporate) or July 2027 (self-employed). Confirm with your vendor that their compliance roadmap is on track.

For B2B e-invoicing, your business needs to generate EN 16931-compliant structured invoices, connect to AEAT’s public platform or a certified private platform and handle invoice status reporting and payment date transmission.

Data readiness is where most teams underestimate the work. Customer and vendor master files need accurate tax identification numbers (NIF/CIF), your invoice templates need to support structured format fields and your payment workflows need to capture and transmit payment dates to the platform.

Workflow ownership

B2B e-invoicing in Spain touches more teams than typical compliance projects:

- AR teams own outbound invoice accuracy, format compliance and status monitoring

- AP teams must respond to incoming invoices (accept/reject) and ensure payment dates are reported

- Tax teams manage SII reporting, VeriFactu compliance and the overlap between regimes

- IT teams handle platform connectivity, software certification and integration between ERPs and the public or private e-invoicing platform

Readiness checklist

Use this checklist as a starting point for tracking your preparation across all three mandates:

- Map your regime exposure: Determine which of SII, VeriFactu, B2B e-invoicing and B2G apply to your business.

- Confirm VeriFactu software compliance: Verify your e-invoicing software vendor’s certification timeline against January/July 2027 deadlines.

- Audit master data quality: Validate NIF/CIF numbers, addresses and tax classifications in customer and vendor records.

- Evaluate platform options: Compare AEAT’s public solution against private platforms based on your invoice volume, trading partner landscape and ERP integration needs.

- Design status reporting workflows: Build processes for AP teams to accept and reject invoices and for payment dates to flow to the platform automatically.

- Plan for dual-format transition: If it applies to your business, prepare to send PDF copies alongside e-invoices during the period before smaller recipients are required to receive structured invoices.

- Coordinate across regimes: Ensure SII reporting, VeriFactu records and B2B e-invoicing don’t create duplicate or conflicting data submissions.

How to avoid compliance risk when implementing e-invoicing in Spain

Spain’s overlapping regimes create specific failure modes that finance teams should anticipate.These are the most common mistakes and how to avoid them when it comes to implementing Spain’s new e-invoicing mandates.

Zone & Co is monitoring e-invoicing developments across Europe, including Spain, as requirements continue to evolve. Businesses with Spanish entities should begin assessing their invoice workflows, data readiness and compliance obligations now, while confirming final requirements with local tax advisors or official AEAT guidance.